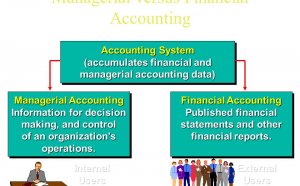

Financial versus Managerial Accounting

While managers are responsible for the efficient operation of a business, accountants are responsible for reporting the results of that effort to the investment community. With these two key points in mind, the difference between financial and managerial accounting is much easier to understand.

In this article, we're going to explain the difference between managerial accounting, also known as management accounting, and financial accounting. We'll start that discussion by talking about the overall objectives of accountants versus managers. Next, we'll talk about the types of reports produced by each group, and how that information is used both internally and externally. Finally, we'll provide a table that summarizes the difference between managerial and financial accounting reports.

Managerial and Financial Accounting

The objective of the financial accounting department is to provide investors, and governing bodies, with a historically accurate report of a company's financial condition. End users of financial accounting reports include investors and creditors, as well as government / regulatory agencies. For example, financial accounting reports are sent to government agencies such as the Internal Revenue Service as well as the Securities and Exchange Commission.

The objective of managerial accounting is to provide internal decision makers with data they can use to control, or improve, the operation of the business. A management report, such as a budget, is used by line managers to understand how their individual operating unit is contributing to the profitability goals of a company. In general, financial accounting reports are externally focused, while managerial accounting reports have an internal focus.

Financial Accounting Reports

Financial and managerial accounting processes will also differ in the types of reports produced by each group. Financial reports provide their end users with a holistic and historical account of the company's financial health. These reports will also follow a fairly narrowly defined format and approach. For example, these reports will record data as prescribed by GAAP, or Generally Accepted Accounting Principles.

The most commonly compiled financial accounting reports include:

These reports are used by investors, creditors, and regulators to assess the financial wellbeing of an organization.

Managerial Accounting Reports

As previously mentioned, managerial reports are internally focused. They can provide the end user with both a historical account of a business operation's performance as well as a forward-looking forecast. Reports are typically prepared on a weekly or monthly basis by managers or business analysts. While the structure of the report is not prescribed by a governing body, the data contained in the report will often be gathered using a statistical approach, and provide readers with variance explanations.

Some of the more commonly compiled managerial accounting reports include:

- Sales and Revenue Forecasts: includes forecasts of unit volumes (sales), as well as the dollars (revenue) associated with those sales. Variance explanations usually accompany sales and revenue forecasts.

- Budget Forecasts and Variance Explanations: these forecasts often use a cost accounting or activity-based cost technique. Actual budget results are compared to original plans as well as forecasts. Variance explanations usually accompany revised forecasts.

Managerial reports are used by supervisors, line managers, process owners, as well as executives, to gain a better understanding of the current financial and operational health of their organization. The information is used to identify areas where there might be an opportunity to improve the efficiency of a business unit or group. Data in these reports tend to be more "granular" in nature, examining performance down to the departmental level.

Summary Table

We're going to finish this topic by providing a table that summarizes the high-level differences between financial and managerial accounting approaches and reports.

Financial and Managerial Accounting Differences

| Financial | Managerial | |

| Purpose | Reporting of Results | Plan, Control, Improve Operations |

| End Users | Regulators, Investors, Creditors (External) | Line Managers, Executives (Internal) |

| Time Dimension | Historical, Actual Results | Plans, Actual Results, and Forecasts |

| Structure | Prescribed by Regulators | Based on Business Needs |

| Information | Company / Enterprise Level | Down to Individual Operating Unit |

| Data Verification | Independent Audits | Internal Controls |

YOU MIGHT ALSO LIKE

Share this Post

Related posts

Managerial versus Financial Accounting

Managerial accounting provides internal reports tailored to the needs of managers and officers inside the company. On the…

Read More

Financial VS Managerial Accounting

Jeffrey Glen Within accounting there are two key fields that relate to different aspects of the businesses finances, financial…

Read Morelatest post

-

Relevance in Financial Accounting November 29, 2017

Relevance in Financial Accounting November 29, 2017 -

Financial Accounting Careers November 26, 2017

Financial Accounting Careers November 26, 2017 -

Financial Accounting Standard Setting in the United State November 23, 2017

Financial Accounting Standard Setting in the United State November 23, 2017 -

Dell Financial account November 20, 2017

Dell Financial account November 20, 2017 -

LPL Financial my account November 17, 2017

LPL Financial my account November 17, 2017 -

Learn Financial Accounting November 14, 2017

Learn Financial Accounting November 14, 2017 -

Financial statements definition in Accounting November 11, 2017

Financial statements definition in Accounting November 11, 2017 -

Financial Accounting for non Profit Organizations November 8, 2017

Financial Accounting for non Profit Organizations November 8, 2017 -

Financial Accounting Programs November 5, 2017

Financial Accounting Programs November 5, 2017