Financial Accounting Standards Board History

Since 1973, the Financial Accounting Standards Board (FASB) has been the designated organisation in the private sector for establishing standards of financial accounting and reporting in the United States of America. Those standards govern the preparation of financial reports. They are officially recognised as authoritative by the Securities and Exchange Commission (Financial Reporting Release No. 1, Section 101) and the American Institute of Certified Public Accountants (Rule 203, Rules of Professional Conduct, as amended May 1973 and May 1979).

The stated mission of the Financial Accounting Standards Board is to establish and improve standards of financial accounting and reporting for the guidance and education of the public, including issuers, auditors, and users of financial information.

FASB Codification

Effective 1 July 2009, the FASB reorganised its standards into the FASB Codification. The Codification is an online research system representing the single source of authoritative nongovernmental US GAAP. Subscriptions to the FASB Codification are available in two ways:

- Professional view, which provides topically organised access to all authoritative nongovernmental US GAAP, including relevant SEC content, with a wide range of supporting utilities including text searching, cross-references, and access to previous versions of content. Annual subscription is US$850 for a single concurrent use. Accounting educators and students can get free access.

- Basic view, which provides topically organised access to all authoritative nongovernmental US GAAP, including relevant SEC content, with limited supporting utilities. Available at no charge.

YOU MIGHT ALSO LIKE

Share this Post

Related posts

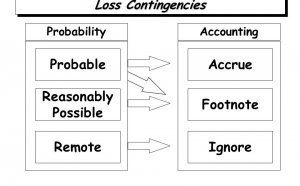

Financial Accounting Standards No. 5

Presentation Chapter 13-1 Current Liabilities and Contingencies

Read More

Financial Accounting and Analysis notes

Financial analysis (also referred to as financial statement analysis or accounting analysis or Analysis of finance) refers…

Read Morelatest post

-

Relevance in Financial Accounting November 29, 2017

Relevance in Financial Accounting November 29, 2017 -

Financial Accounting Careers November 26, 2017

Financial Accounting Careers November 26, 2017 -

Financial Accounting Standard Setting in the United State November 23, 2017

Financial Accounting Standard Setting in the United State November 23, 2017 -

Dell Financial account November 20, 2017

Dell Financial account November 20, 2017 -

LPL Financial my account November 17, 2017

LPL Financial my account November 17, 2017 -

Learn Financial Accounting November 14, 2017

Learn Financial Accounting November 14, 2017 -

Financial statements definition in Accounting November 11, 2017

Financial statements definition in Accounting November 11, 2017 -

Financial Accounting for non Profit Organizations November 8, 2017

Financial Accounting for non Profit Organizations November 8, 2017 -

Financial Accounting Programs November 5, 2017

Financial Accounting Programs November 5, 2017